- Zenith Newsletter

- Posts

- Get the hedge funds out of your hedges

Get the hedge funds out of your hedges

All about houses: the state of the market, when to buy (and when not to), hedge funds buying up starter homes, and renting your house to your business tax-free.

Jon Scott, Bennett Fees & Nate Hoskin

December 22, 2023

The attempt to get hedge funds out of your hedges

Over the past week and a half, Congress introduced two bills combating hedge funds who buy residential homes. The first bill—named “End Hedge Fund Control of America Homes Act” was introduced by two Senate Democrats, Jeff Merkley of Oregon and Adam Smith of Washington. Here’s a summary:

“The End Hedge Fund Control of American Homes Act seeks to put an end to this harmful practice of hedge funds buying up single-family homes by banning hedge funds from owning these types of homes and requiring them to sell at least 10% of the total number of single-family homes they currently own to families per year over a 10-year period. After a 10-year full phase-out, all hedge funds will be completely banned from owning any single-family homes.”

Two North Carolina Congressional Democrats introduced the “American Neighborhoods Protection Act” which will “require corporate owners of more than 75 single-family homes to pay an annual fee of $10,000 per home into a housing trust fund to be used as down payment assistance for families.”

Hold your horses though because there are some real roadblocks here. First, both these bills face a steep uphill climb for passage. Republicans still control the house, and it is unlikely that the GOP will pass what are so far solely Democratic sponsored bills. The second problem, according to experts, is the real issue causing unaffordable housing lies with homebuilders who have been building far fewer homes than in previous decades.

Either way, housing affordability is clearly a conversation that needs to happen in this country (and in Canada).

The state of the housing market

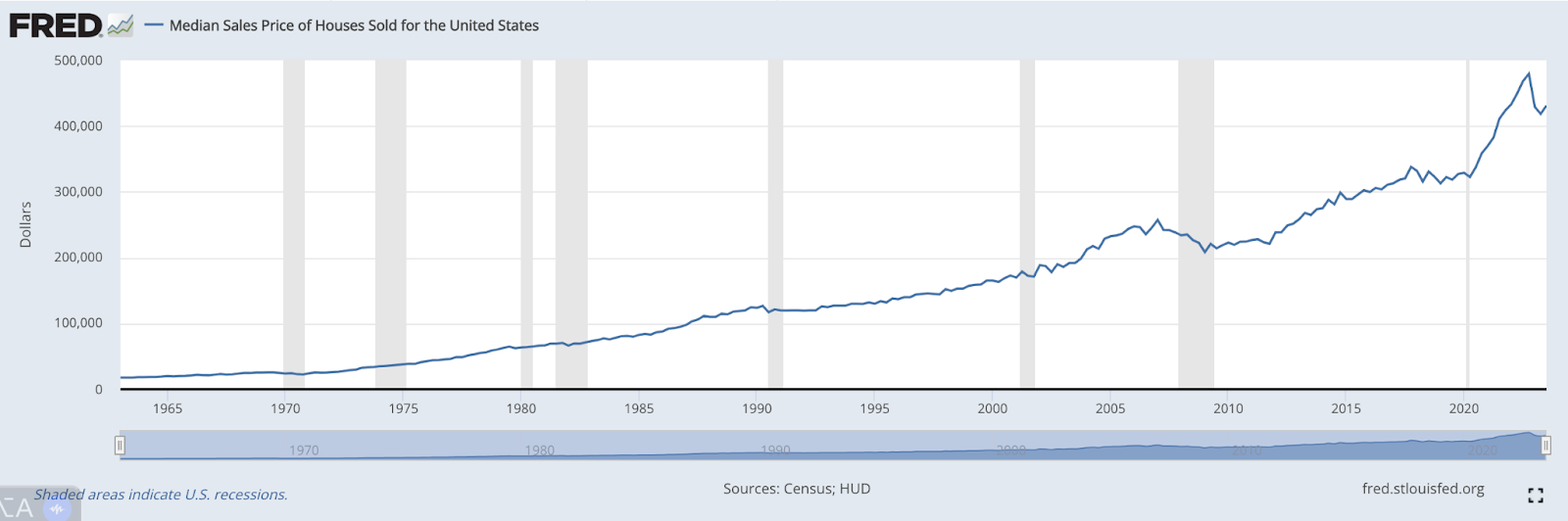

Houses are expensive. Take this chart below showing the median home price.

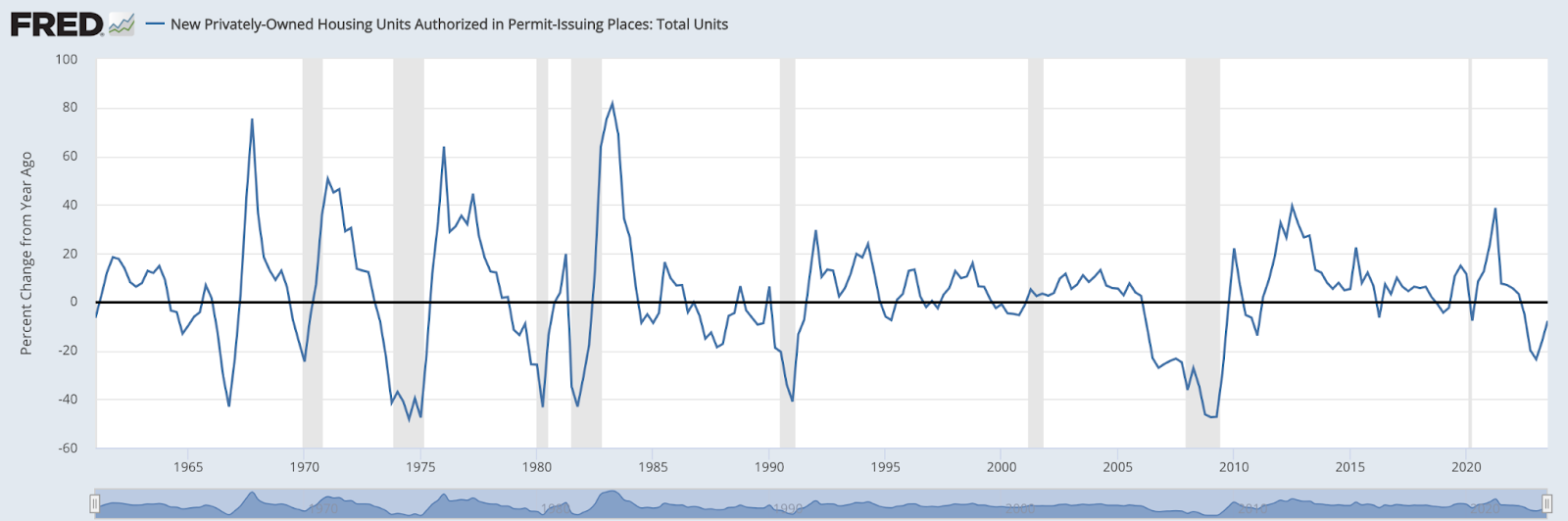

While prices are down from their peak in Q4 2022, they are still extremely elevated. With demand for houses staying relatively strong, it is housing supply that remains constrained. This makes sense, with higher interest rates, the cost of borrowing increases making larger investments like building a home more expensive. To take one, historically accurate leading indicator of the housing market, new permits, we saw a negative 20% year-over-year decline in new permits, a level which almost always indicates a recession as shown by the grey bars.

So what does this mean?

This recent increase in permits as well as the decrease in mortgage rates, and the recent increase in existing home sales all lend themselves to a slightly more optimistic outlook than has dominated the minds of analysts for most of the year. That said, housing supply is a much larger issue affected by many more factors than just interest rates so the extent that the housing market will loosen is still unclear.

Is now the time to buy a house?

The housing market in 2023 sucked, with stubbornly high mortgage rates and rising home prices making it nearly impossible to justify buying over renting.

However, the Federal Reserve recently decided to leave interest rates unchanged AND project rate cuts in 2024.

Here’s the problem: with housing supply so tight (see above), falling interest rates may cause home prices to shoot up even further, outweighing the benefits of lower mortgage rates.

So… when do I buy?

The short answer is when you can afford it. Buying now puts you on the right side of the “affordability crisis” and, if lower interest rates do cause home prices to jump, you get to build equity and take advantage of homeownership benefits like tax deductions and home equity lines of credit. That said, unless you plan to stay in the home for the long term (5-7 years at a minimum), buying is rarely a wise financial move.

So… I should wait?

Don’t buy until you find the right home, within your price range, in a place you can stay for the long term. Focusing on preparing financially while waiting will set you up for success. Being house-poor is a very, very real thing and can ruin your sense of financial security if it’s not planned for.

Remember, the goal shouldn't be perfectly timing the market; it should be to prioritize your personal needs, financial situation, and the right home for you.

Rent your house to your business tax-free

If you have a side hustle or a business, you can rent your house to your business for up to 14 days a year completely tax free.

Thanks to the Augusta rule, homeowners don’t need to report rental income if the house is rented out for 14 days (or less) per year.

This means you can rent your house to your business (which claims the expense as a tax deduction) and you don’t have to pay any taxes on the income!

The game still has rules:

Your business cannot use your home as its primary business address or “place of business”.

You cannot claim the home office deduction AND the Augusta rule (refer to rule 1).

The rent must be reasonable for your location, size of home, etc.

You need to keep your records. Record the quotes for nearby meeting spaces to prove the rent you charged was reasonable and keep minutes of meetings held at your home to prove work was actually done on premises.

The business must be a Partnership, an LLC taxed as a Partnership, an S-Corp, or C-Corp. It cannot be a Sole Proprietorship or a Single-Member LLC.

If the total rent paid exceeds $600, the business must issue a 1099-MISC to you as an individual even though the income is not reportable.

The Augusta Rule is a great way to move money from your business to yourself tax-free.

As always, these are never “one size fits all” and we always recommend getting in touch with us or other professionals before implementing this in your own business.

What shouldn’t happen at tax time

While a big tax return seems like a good thing… it actually is not. The reality is a large tax return means you were taxed more during the year than you should’ve been. So while you were carefully budgeting out your paychecks all year, there was actually extra money you could have saved or used.

Now I can hear the comments (if this newsletter had comments) that some of you are going to stash away your refund in your savings or invest it, so a large refund isn’t a huge deal. Well it’s still a problem, because money loses value over time. Therefore, if you would’ve had your future refund during your actually paychecks during the year you could’ve invested that money or stashed it in a High Yield Savings Account. In fact, if you missed out on investing your refund during the year you should especially be kicking yourself, since the S&P 500 and Nasdaq has grown 20%+ and 40%+, respectively, year to date. This has been a banner year for the indexes so safe to say you have missed out if you’re not investing that money until you receive your refund.

Luckily, planning your tax withholdings is something Hoskin Capital can help you with.

Work with Hoskin Capital

Knowing is half the battle, we help you get it done.

We manage your entire financial life for a fixed annual fee.

Meet our team of experts, peep our services, and learn why we exist.

In case you missed them… here are our house-related TikToks:

@natehoskin Save $10,000 when buying your first house #homebuyertips #homebuying #firsttimehomebuyer #financialliteracy #financialeducation #financial... See more

@natehoskin Replying to @evneli Take 1 of this skit #homebuyer #homebuyertips #fyp #viral #financialfreedom #finlit #personalfinance #financialliteracy

@natehoskin A case FOR buying a house! Like and follow to see the case AGAINST buying a house tomorrow 👀 #homebuyer #realestate #financialliteracy #fi... See more

@natehoskin Replying to @user349703446552 a case for NOT buying a house! #homebuyer #realestate #finlit #financialfreedom #financialliteracy

Be greedy when others are fearful. Be fearful when others are greedy

Reply