- Zenith Newsletter

- Pages

- Understanding different investment accounts

Understanding different investment accounts

By Katie Martens

Abstract: The different types of retirement investment accounts and how to open an account.

Did you know that employee 401Ks only got their start in the 1970s, making it a fairly new phenomenon?

The 401K is a retirement plan offered by employers. Roughly 40% of employers have them and they are by far one of the most popular retirement investment accounts. Before the 401K, some people were lucky to be employees with fixed pension plans at the same company for their entire working lives. When that employee retired, the company continued paying a fraction of that salary to the retired employee until they died. Everyone else who was not as lucky to have this pension (only about ⅓ of American workers had a pension) survived on Social Security and savings.

The difference between 45 years ago and today is that back then, people didn’t live that long after retirement. ERISA changed the landscape of those who had pensions and those who did not in 1974. ERISA stands for Employee Retirement Income Security Act of 1974. This Act forced companies to actually recognize how expensive those pension plans were because the Act forced companies to put money aside for these pensions to fund the pensions properly. Combined with Americans living longer, companies found these pension plans too expensive to maintain, so they began to no longer offer them, leaving a hole in the marketplace for defined retirement plans.

The 401K was developed in the late 1970s and refers to the section of the IRS code that it derives authority from. It allows employees to contribute a portion of their paycheck tax-free, and employers are allowed to match those contributions, and those matches are tax deductible. This section of the tax code allows employers to offer a real perk to inspire loyalty, and is far less expensive than pension plans. Additionally, it allows people to save for retirement effortlessly, with automatic deductions coming from their paychecks.

Today, Americans have over $5 trillion in 401K plans. In this article, we’ll be discussing the different retirement accounts available, and how to decide what will ultimately work best for your situation.

Retirement Accounts

Generally, there are three investment vehicles people use for retirement:

401K

As discussed earlier in the article, 401Ks allow employees to contribute a portion of their wages to an individual account, and the employer can choose to match up to a certain percentage. The portion that the employee chooses to set aside into a 401K is not taxed as income, but when the money is withdrawn from the 401K, it is taxed as income.

Traditional IRA

IRA stands for “Individual Retirement Account” and there are a few types of IRAs. A traditional IRA is a tax-advantaged personal savings plan where contributions may be tax deductible, depending on your filing status and income. Generally, amounts in a traditional IRA are not taxed until you take a distribution (another word for distribution is “withdrawal”) from your traditional IRA.

Roth IRA

Roth IRAs are a tax-advantaged personal savings plan where contributions are not deductible but qualified distributions may be tax free. Here are the differences in a Roth IRA compared to a traditional IRA:

You can’t deduct contributions to a Roth IRA

If you satisfy the requirements, qualified distributions are tax-free

You can make contributions to your Roth IRA after you reach age 70.5

You can leave amounts in your Roth IRA as long as you live

The account or annuity must be designated as a Roth IRA when it is set up

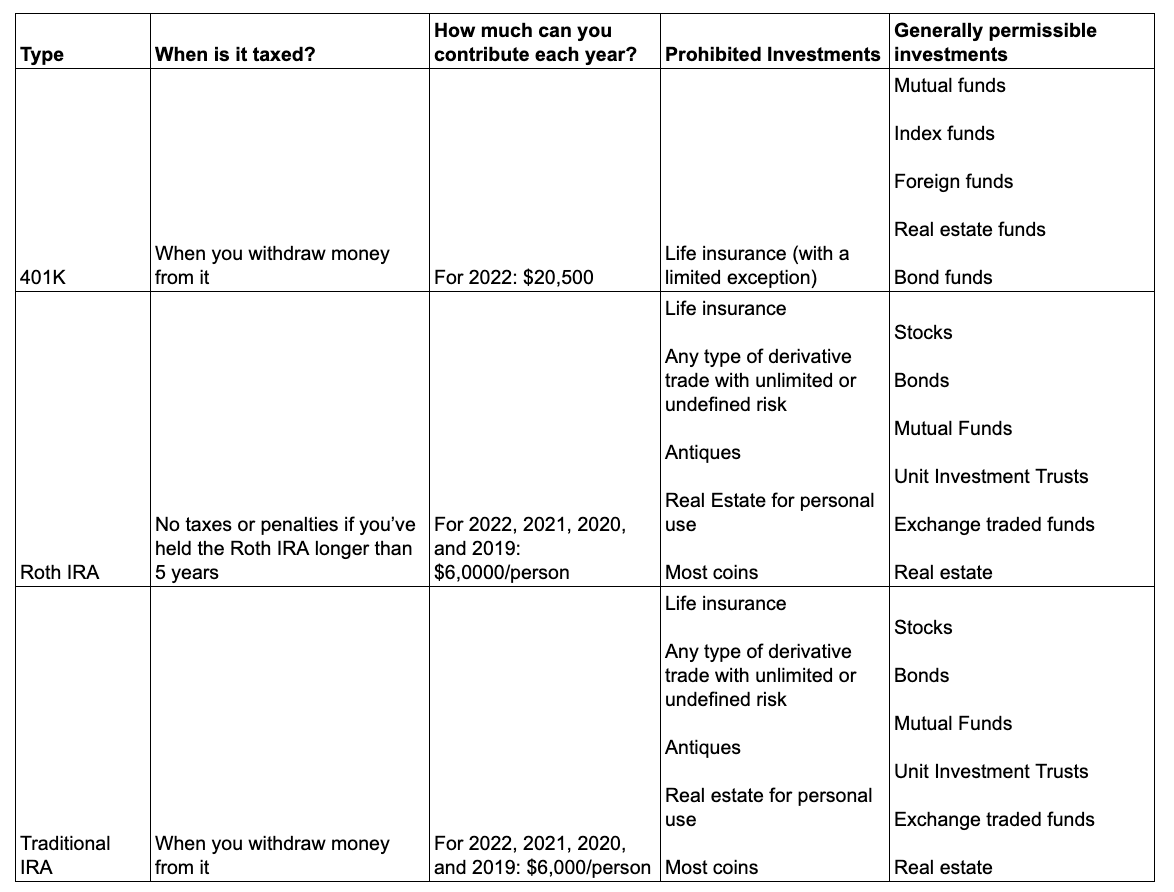

Comparing Retirement Investment Account Types

The following chart is meant to help you easily identify the differences between each retirement account vehicle. It’s important to remember that the amounts you can contribute to each account varies each year, for example, the IRS allowed up to $19,500 to be contributed to 401K plans in 2022, and in 2023 allows up to $22,500.

Choosing the Account that Matches the Investment Goal

So which one should you do? Like many things in life, like whether you should buy a house, or whether you should have a second cookie, your investment choices are going to look different from person to person.

Factors to think about:

Your savings goal (for example, do you want to retire in your 50s? Or would you rather work until you’re dead?);

Your eligibility for certain investment accounts;

Who do you want to retain ownership of the account? (You, you and someone else, or even a minor)

The table below compares the 4 different investment accounts that you could set up:

Where should you open your investment account?

Most financial institutions offer, at a minimum, standard brokerage accounts and IRAs. Many also offer education savings accounts and custodial accounts.

If you want to pick and manage your investments on your own, opening an account at an online broker is the way to go. Here is a small list of a few online stock brokers:

Fidelity

Merrill

Vanguard

E*Trade

Ameritrade

If the thought of opening an account with online brokers and doing everything yourself is too much, there are robo-advising services and personal brokers who can guide you to the investment vehicle that works best for you, at whatever stage of life you’re in.

A robo-advisor is a service that provides automated investment advice and management based on proprietary software and algorithms. Customers generally start using the service by filling out surveys that determine goals, risk tolerance, and time horizons. The company will use its own software to determine the appropriate asset allocation and will give advice to the customer on when and how much they will need to contribute to meet their goals.

Once the robo-advisor has assets under their management, they usually will periodically use an automated process to rebalance the portfolio to meet designated metrics for performance and potentially do some tax-loss harvesting. Companies that offer robo-advising include:

Wealthfront

Betterment

M1 Finance

E*Trade

Interactive Advisors

Finally, there are humans who can serve as your financial advisor. You’d likely meet in person, discuss your financial goals, and the advisor would give you guidance on what investment accounts would serve you best. If you’d feel better investing your money under the guidance of a real, live person, this option would probably work best for you. There are thousands of financial management companies, so providing a list would be a bit of a disservice to pointing you in the right direction. Finding the right financial advisor is a lot like finding the right doctor, the right dentist, or the right lawyer for your situation: do you feel comfortable being candid with them? And do you feel that they are candid with you? If you don’t feel comfortable, trust yourself and your ability to find someone else. It is, after all, your money at stake.